We’ve talked a lot already about where stuff comes from, but we need to talk about why there is a supply. Typically, demand gives rise to supply. If entrepreneurs and business people see that there is a need for something, someone will invariably invent it, produce it and sell it.

We all want and need goods and services. And we all have different ideas about how much we are prepared to pay. We could also say that we “demand” goods and services, or that we have a willingness to pay for stuff.

The theory of demand is all about consumers and states that as prices rise, consumers will demand less, or that quantity demanded will fall. Consider yourself. If you are a student, you likely don’t have much disposable income after you pay for tuition and books. So, what do you typically eat? When I went to school decades ago, most students ate rice and noodle soup. Or, Kraft Dinner. When the local grocery store had a 50% off sale, students would stock up! Rather than buying five boxes of KD, most students would buy 10 or 15 or even more to save money. This makes sense because money is a scarce resource and if you can get more for less, why wouldn’t you?

Let’s look at another food example: sausage. Table 1 illustrates the demand for sausage from three different individuals. Notice that demand falls for each person as the price rises.

You’ll also notice that each person will buy different amounts at each price. Why do you think that is? It could be taste – perhaps Carl doesn’t like sausage as much as Adam. Maybe Adam has a higher income and can afford to eat more meat. We will explore a bunch of reasons that could explain the differences.

Table 6-1: Sausage demand (#) by price ($/kg). Permission: Courtesy of course author Hayley Hesseln, Department of Agriculture and Resource Economics, University of Saskatchewan.

Each person demands less (more) as the price rises (falls). We can graph the demand curve as all the price/quantity combinations in Table 1. When we do this, we get a downward-sloping individual demand curve for each person showing an indirect relationship between price and quantity demanded (adverse meaning that as price rises, quantity demand decreases and vice versa).

Figure 6-1: Individual demand curves for sausage. Permission: Courtesy of course author Hayley Hesseln, Department of Agriculture and Resource Economics, University of Saskatchewan.

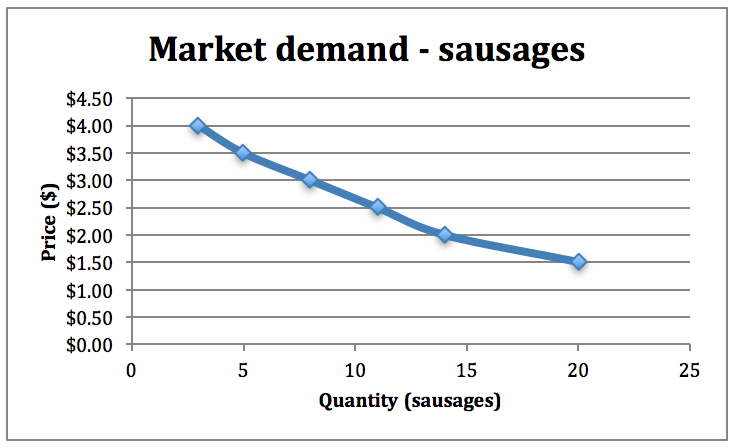

Let’s now look at the market demand. If we assume there are only three individuals in our market, we would add up the total quantity demanded at each price. We could do this if there were 100 people in the market, or 1,000 or more. We make an assumption here that one individual cannot influence the price by purchasing large quantities. Therefore, we assume these consumers are price takers.

At a price of $4/kg, the total demand is 2 + 1 + 0 = 3. If the price drops to $3.50/kg, we see that quantity demanded increases. To calculate the market demand we add each quantity at the price of $3.50 à 3 + 2+ 0 = 5. We continue to do this and then plot the total quantity demanded at each price to arrive at the market demand for sausages (assuming a tiny three-person market).

Figure 6-2: Market demand for sausages. Permission: Courtesy of course author Hayley Hesseln, Department of Agriculture and Resource Economics, University of Saskatchewan.

Something to note: the market demand curve is also downward sloping, indicating that in general, as prices fall, the quantity demanded increases. Think of all the sales after Christmas… the lower prices are sure to clear the shelves, as people are more willing to shop for bargains. Now, let’s go back to production.